This study investigates the techno-economic potential of green hydrogen production in Mongolia, and its application in three hard-to-abate end-use sectors - namely heavy-duty transport in the mining sector, public transportation in Ulaanbaatar, and decentralised space heating and cooking. Based on the results, the GHG emission reduction potential is estimated, followed by an analysis on potential policy options for the introduction of green hydrogen in the Mongolian context.

Main findings:

Despite Mongolia’s rich renewable energy resources, some hard-to-abate sectors are technically challenging to electrify, and other decarbonisation options needs to be considered. The climatic conditions in Mongolia, particularly in the South Gobi region, provides the country with favourable conditions for green hydrogen production. This study investigates the techno-economic potential of producing and applying green hydrogen in three end-use sectors including heavy-duty transport in the mining sector, public transportation in Ulaanbaatar, and decentralised heating in ger districts.

We find that green hydrogen could be produced relatively affordably, at 3.3-4.7 USD/kg of hydrogen – compared to a global average of 4.8 USD/kg in 2020. The most optimal location for green hydrogen production with respect to the cost effectiveness is in the South Gobi region. However, its production potential may be limited by the local availability of water resources which is already scarce in the southern region of the country.

From the demand side analysis, the results suggest that heavy-duty transport in the mining sector is the most promising application when considering both economic feasibility and GHG emission reduction potential. Shifting to a fuel cell-based truck fleet in 2020 would only be 12% more expensive compared to purchasing and operating new diesel trucks, in terms of energy delivered to the wheel. Shifting to fuel cell trucks in the complete copper and half of the iron ore production in the country could mitigate about 1.2 Mt CO2e annually, corresponding to about 3.5% of national emissions in 2014, at an estimated abatement cost of only 10 USD/tCO2e.

Operation costs of mining vehicles in Southern Mongolia

Operation costs of mining vehicles in Southern Mongolia

As most mining activities are located in the South Gobi area, green hydrogen can be produced at lowest cost close to the end-use site and therefore has the advantage of not having to develop any transportation infrastructure for the green hydrogen, which otherwise could significantly impact the cost-effectiveness. The study further finds that, as few alternative decarbonisation technologies are available for this end-use application, fuel cell trucks should be promoted by technology specific policies such as the allocation and distribution of public finance for R&D and piloting. Public-private partnerships could test and demonstrate the technology to build interest among private stakeholders.

In the second case study analysis, a shift to fuel cell public transportation buses in Ulaanbaatar is considered, comparing to the purchasing of new diesel buses. The results suggest that such shift would be only 15% more expensive than purchasing and operating new diesel buses. As the bus fleet is relatively small, and since there are few other urban areas in the country with a significant public bus fleet, the scalability and mitigation potential is limited, amounting to about 39 ktCO2e annually, at an estimated abatement cost of above 100 USD/tCO2e.

Given that, in the case of buses, there are other alternatives to decarbonisation in addition to green hydrogen, policymakers could take a more technology neutral approach which incentivises various decarbonisation technologies equally. Through applying policies such as tax exemptions, purchase grants and vehicle emission standards could engage the private sector to identify the most suitable technology. Alternatively, the comparatively small-scale nature of the sector could make for a useful demonstration project to support the further development of green hydrogen technologies for other applications, as well as in neighbouring countries.

Lastly, we estimate the techno-economic potential of using green hydrogen for decentralised heating and cooking, using LPG as the benchmark fuel. At present, green hydrogen is not cost competitive as it would be 148% more expensive than LPG and is therefore not considered a feasible option in the near term. Nevertheless, Mongolia’s heating sector remains highly emissions intensive and is likely to require some form of seasonal energy storage to fully decarbonise in the long term. Green hydrogen should thus not be completely ruled out as a long-term option but should be part of future potential technology portfolios.

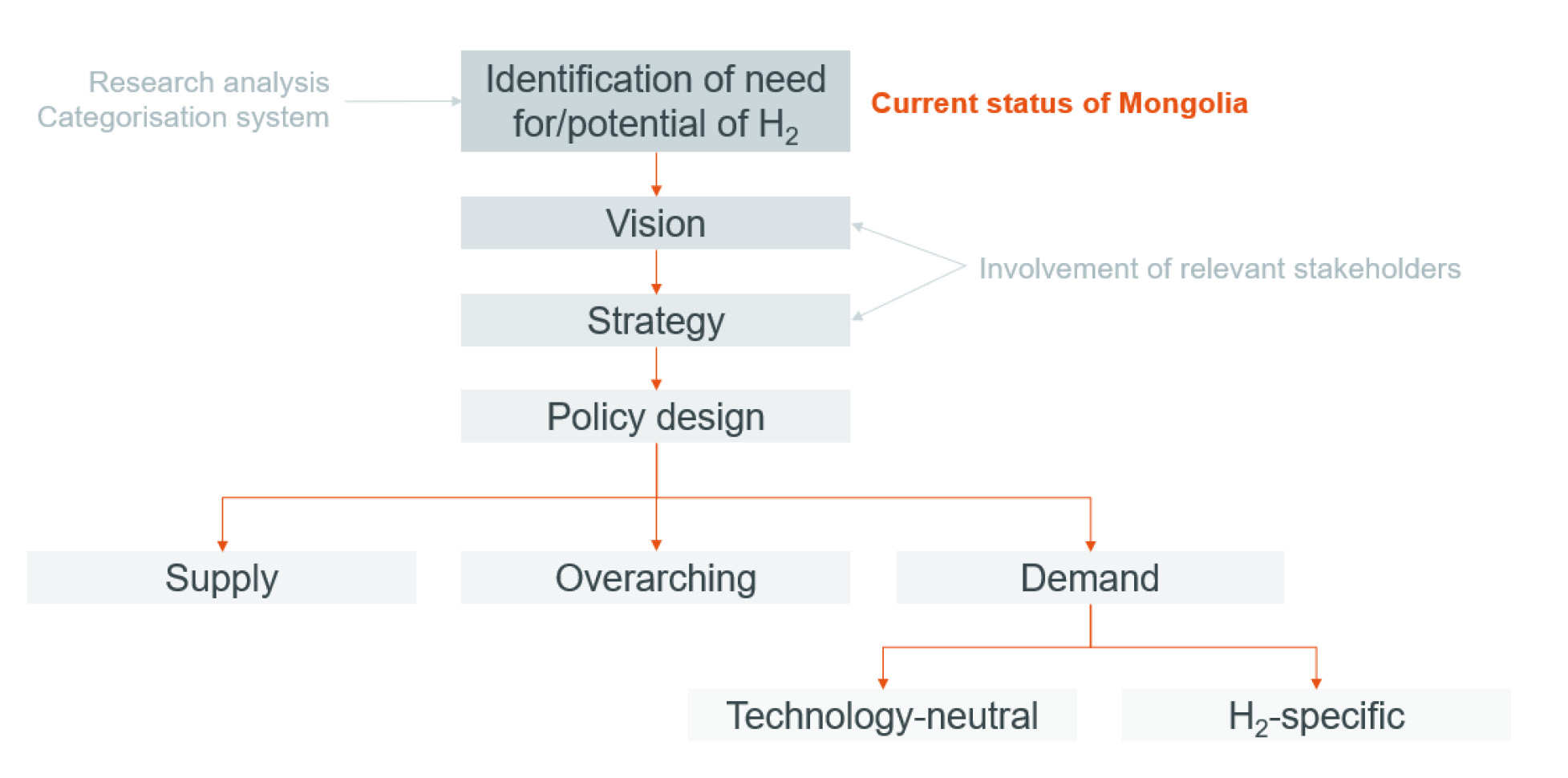

The techno-economic assessment conducted in the study provides a first attempt to identify the potential added value a green hydrogen sector could bring Mongolia. Based on that, a stepwise methodology is suggested for the development of a national green hydrogen vision, and the subsequent formulation of specific policies on the supply and demand sides.