The plastics sector is a major driver of climate change, accounting for 3–5% of global greenhouse gas (GHG) emissions – a share comparable to the aviation sector. With plastic production expected to double, or even triple, by 2050 without intervention, urgent action is needed to reduce lifecycle emissions and align the sector with a 1.5°C-compatible pathway.

Against this backdrop, this report provides a comprehensive analysis with three objectives:

- mapping GHG emissions across the plastics value chain,

- sequencing mitigation strategies to achieve a 1.5°C-aligned plastics sector and

- assessing policies and actions in four major players with different circumstances on plastic production, consumption and recycling (China, the European Union, Saudi Arabia, and the United States) to identify critical gaps and possible ways forward.

Key messages

Plastics as a cause of both climate change and environmental pollution

GHG emissions from plastics are a major driver of exacerbating climate change. 90% of plastics-related GHG emissions stem from the production phase, largely driven by fossil feedstocks and energy-intensive processes like steam cracking.

Plastics also contribute heavily to environmental degradation and health risks, with microplastics found in nearly all ecosystems and in human bodies.

This twin crisis – climate change and pollution – demands integrated solutions.

Sequencing strategies for net-zero emissions plastics

The report outlines the key role that sequencing plays, starting with proven measures that cut emissions now while preparing for longer-term solutions. The report proposes a sequenced approach for transforming the plastics sector, based on three strategies:

- Strategy 1: Minimise production through eliminating unnecessary plastic use and substituting with more sustainable alternatives

- Strategy 2: Enhance circularity by scaling up mechanical recycling, supported by chemical recycling

- Strategy 3: Decarbonise production by reducing the use of fossil fuel as a feedstock and as an energy source transitioning to clean energy sources, supported by research, development, demonstration and deployment (RDD&D)

Regional analysis

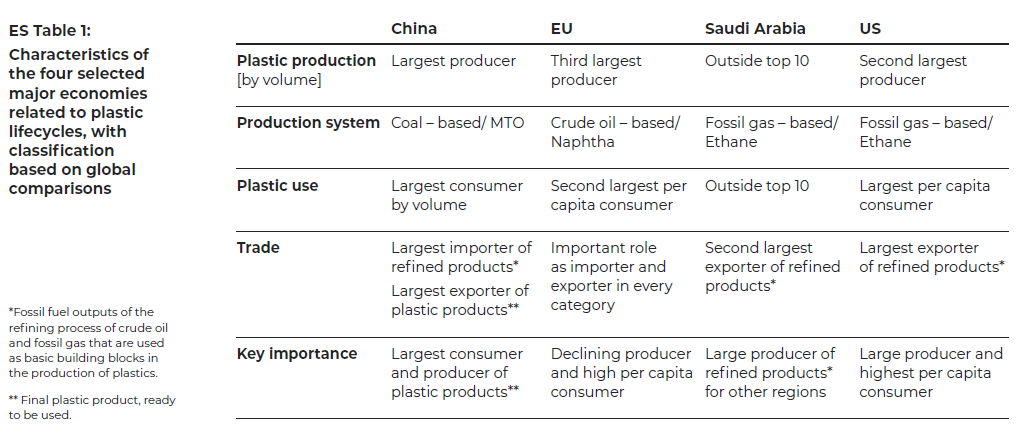

The report analyses China, the European Union (EU), Saudi Arabia, and the United States (US) because they collectively dominate global plastics across all dimensions – fossil extraction, feedstock production, manufacturing, consumption and trade. Each represents a distinct production route and faces unique challenges.

May countries have introduced regulations targeting plastic pollution, primarily aimed at reducing environmental leakage, yet progress remains uneven across regions. Despite increasing attention to plastic pollution, climate-related policies that explicitly address plastics are still limited, and some national strategies risk increasing emissions. Specificity is essential, and decarbonisation policies targeting plastics are needed.

Plastic sector decarbonisation requires systemic transformations, eliminating unnecessary usage of these products and shifting from cheap availability and fast disposability to durability and reuse, especially in high-income countries. Technical solutions need enhanced efforts in RDD&D to accelerate their availability, while avoiding overreliance on silver bullet technological solutions.

Decarbonising plastics: steps towards net zero

Immediate action is needed to reduce plastic production and demand through the reduction of plastic production and consumption, substitution by alternatives to plastics with environmentally sound options and enhanced circularity. Full decarbonisation of the plastic sector requires industrial transformation of the current production systems.

Countries dominating global plastic production and consumption possess the economic and technological capacity to lead decarbonisation of the plastics sector through domestic policy, global cooperation and investment in RDD&D for emerging technologies. Financial and technical support from these regions should be directed to other countries to enable global progress. Tailored decarbonisation pathways must reflect national and regional circumstances, avoiding overreliance on single-technology solutions and supporting the transition toward cleaner, more sustainable production and consumption systems.

The International Legally Binding Instrument (ILBI) on plastic pollution can play a pivotal role by establishing common targets for reducing production and scaling up circularity. At the same time, alignment with the UNFCCC is essential to ensure that plastics feature prominently in national decarbonisation plans, including NDCs and LT-LEDS. Strengthened international cooperation is critical to address both emissions and pollution from plastics, contributing to keeping global temperature rise within 1.5°C.

For further insights, see our Q&A where experts explain why reducing plastics production is essential for effective climate action, drawing on key findings from the full report.