This discussion paper provides input to current standard-setting processes of SBTi, GHG-Protocol and ISO. It assesses the strengths and limitations of current scope 3 accounting approaches and examines examples from big tech companies. It proposes accounting rules that preserve environmental integrity while recognising meaningful climate action in supply chains.

Although current GHG Protocol accounting standards allow market-based accounting only in scope 2, it is common malpractice among big tech companies to also use this approach to account for renewable electricity in their supply chains. This raises transparency and integrity concerns, as their scope 3 emissions reductions may exist only on paper, but not in reality. At the same time, location-based accounting alone does not adequately incentivise high-quality renewable procurement in the supply chain.

Why does this matter now?

GHG Protocol is currently revising its scope 3 guidance and developing a new “Actions and Market Instruments” standard, while the GHG Protocol and ISO are jointly developing a new product-level accounting standard.

Who is this paper for?

This discussion paper is intended for standard setters and stakeholders involved in the revision of corporate GHG accounting frameworks, including the GHG Protocol, ISO and the SBTi. It provides recommendations for strengthening scope 3 and product-level accounting rules, so that they better reflect real-world decarbonisation and incentivise investments in renewable electricity across supply chains.;

What are our key takeaways and recommendations?

- Current GHG Protocol guidance requires location-based scope 3 accounting, but several large technology companies apply market-based approaches, raising transparency and credibility concerns.

- Location-based accounting remains the most robust method for assessing actual emissions and should remain the primary basis for scope 3 reporting.

- Non-GHG transition indicators should be a complementary ledger for scope 3 reporting.

- Market-based accounting paired with hourly matching of renewable electricity should be a complementary ledger for scope 3 accounting.

- Location-based emissions from energy use should be the primary reference point for Product Carbon Footprint (PCF) accounting

- Companies should be allowed to claim lower emissions values only if electricity comes from new Power Purchase Agreements (PPAs) on the local grid and if electricity is matched on an hourly basis

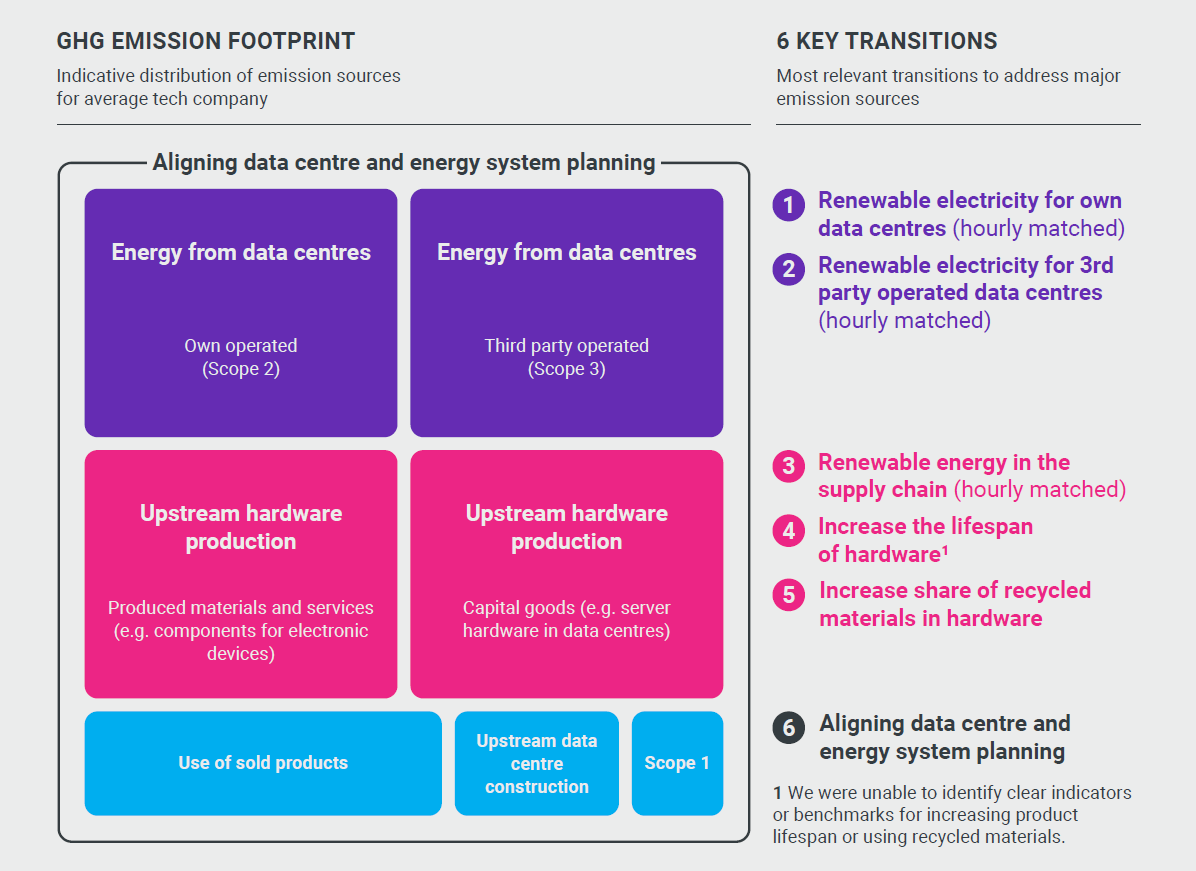

Fig: Emission hotspots in tech companies’ GHG inventory