Update 01 October 2024: VCMI has invited stakeholders to provide feedback on its Scope 3 Claim through a survey, by 07 October 2024.

This document discloses NewClimate Institute’s response to VCMI’s survey, along with an explanation of our interpretation and perspectives.

Summary

- Amid growing controversy over potentially loosening rules for offsetting corporate emissions, the Voluntary Carbon Markets Integrity initiative (VCMI) has launched a consultation period for a second proposal of its contentious Scope 3 Claim.

- VCMI proposes that companies should be able to make extensive use of carbon credits up until 2038 to address the “emissions gap” between their target trajectories and their actual emissions, which would result in weakening the system of accountability for corporate climate action.

- Problem 1: Backsliding ambition | The VCMI proposal risks further undermining already insufficient levels of corporate climate ambition, potentially reverting to marginal, business-as-usual emission reductions.

- Problem 2: Distract from and delay short-term action | The VCMI proposal could enable companies with ambitious-sounding targets to delay meaningful immediate emissions reductions, allowing them to continue increasing their emissions in the short term.

- Problem 3: Undermining efforts of front-runners | The VCMI proposal could disadvantage ambitious companies with genuine climate strategies by allowing laggard competitors to exaggerate their own efforts.

- There are far more transparent and constructive solutions to the challenges companies face in decarbonising their value chains, such as focusing on key emission sources and setting targets that specifically address them.

- We urge VCMI to abandon the proposal of flexibility mechanisms that are not aligned with — and may even undermine — the promising improvements expected in the SBTi’s Corporate Net Zero Standard. Carbon credits should not be used as a flexibility mechanism to suggest that companies are on track to meet their targets, nor as adequate compensation for falling short of those targets.

Amid growing controversy over potentially loosening rules for offsetting corporate emissions, the Voluntary Carbon Markets Integrity initiative (VCMI) is consulting opinion on a second proposal for its contentious Scope 3 Claim

On 02 September 2024, the Voluntary Carbon Markets Integrity initiative (VCMI) launched a consultation period for its Scope 3 Claim. This is a second iteration of VCMI’s proposal, which was first published in November 2023 as the "Scope 3 Flexibility Claim" and which received significant pushback from civil society and the scientific community. The revised proposal comes amid growing controversy over the rules for offsetting corporate emissions.

VCMI’s revised proposal suggests that companies could purchase carbon credits for up to 24% of their target emission levels until 2038 to address the “emissions gap” between their target trajectories and their actual emissions. Whether this constitutes offsetting is subject to interpretation. Although VCMI states that the Scope 3 Claim cannot be used to meet emission reduction targets or to offset scope 3 emissions, the specific terms of the claim remain undefined. We believe it is highly likely that the Scope 3 Claim could mislead investors, consumers and regulators, potentially encouraging companies to use carbon credits as an alternative to cutting emissions within the value chains.

VCMI’s proposal threatens the principle that companies should not be able to achieve short- and medium-term emission reduction targets through offsetting. This has been a cornerstone of the Science Based Target initiative (SBTi) since its initiation and was also one of the key recommendations in the Integrity Matters report by the United Nations’ High-Level Expert Group on the Net-Zero Emissions Commitments of Non-State Entities (UNFCCC, 2023c).

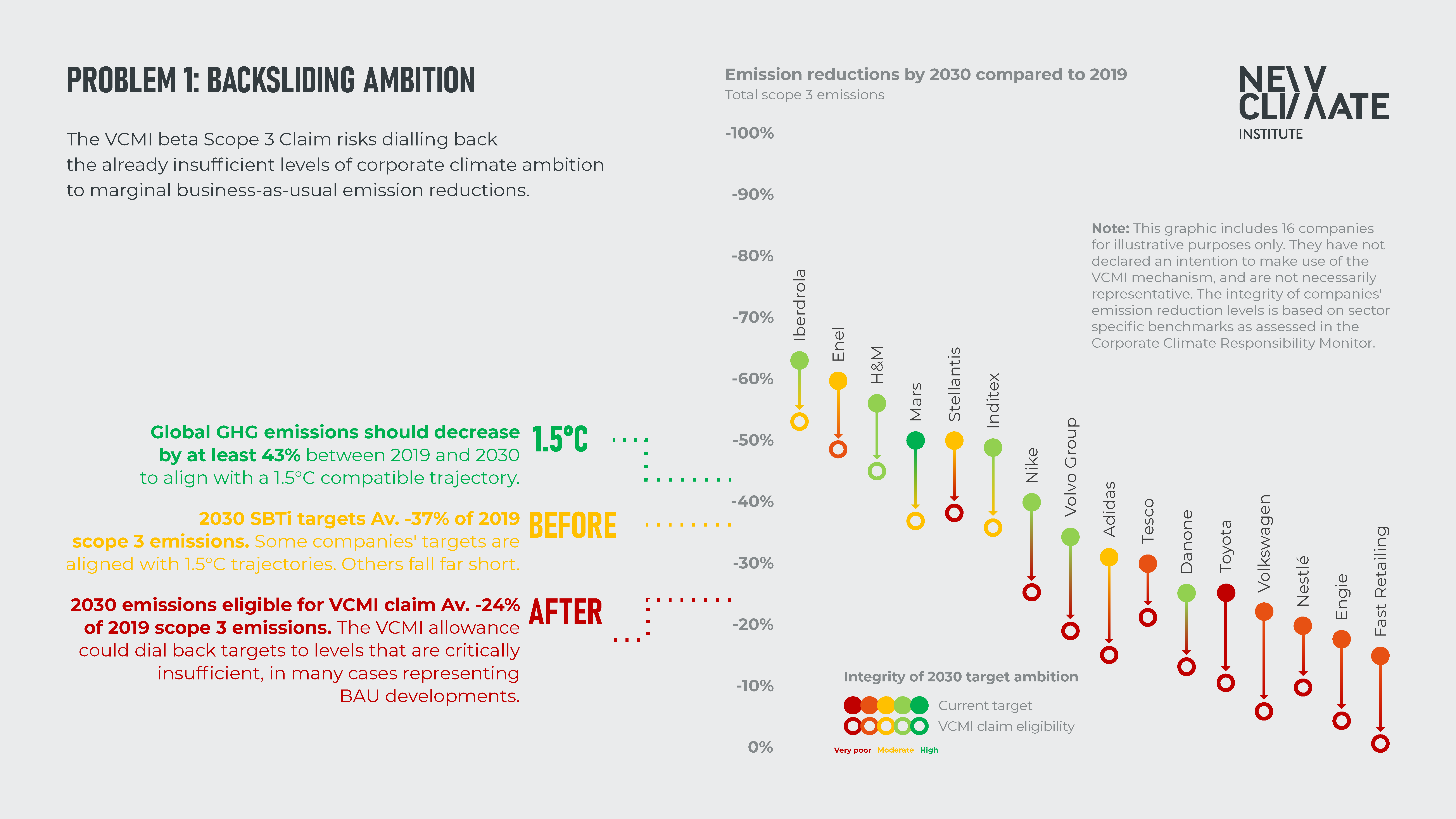

Problem 1: Backsliding ambition

The VCMI proposal risks dialling back the already insufficient levels of corporate climate ambition to marginal business-as-usual emission reductions.

To illustrate the implications of the Scope 3 Claim for existing 2030 targets, we tested it on the 16 companies covered in the 2024 Corporate Climate Responsibility Monitor report that have SBTi-validated 2030 targets for scope 3 emissions.

Figure 1 demonstrates that the revised Scope 3 Claim could further weaken the already insufficient 2030 targets of most companies. The VCMI allowance could reduce scope 3 targets to levels that are critically insufficient for achieving sector-specific trajectories needed to limit global warming to 1.5°C. Some companies would be eligible for the VCMI claim with emission reduction levels so minimal that they essentially represent business-as-usual scenarios, requiring no meaningful climate action.

Note: This graphic includes 16 companies for illustrative purposes only. They have not declared an intention to make use of the VCMI mechanism, and are not necessarily representative. The integrity of companies' emission reduction levels is based on sector-specific benchmarks as assessed in the Corporate Climate Responsibility Monitor.

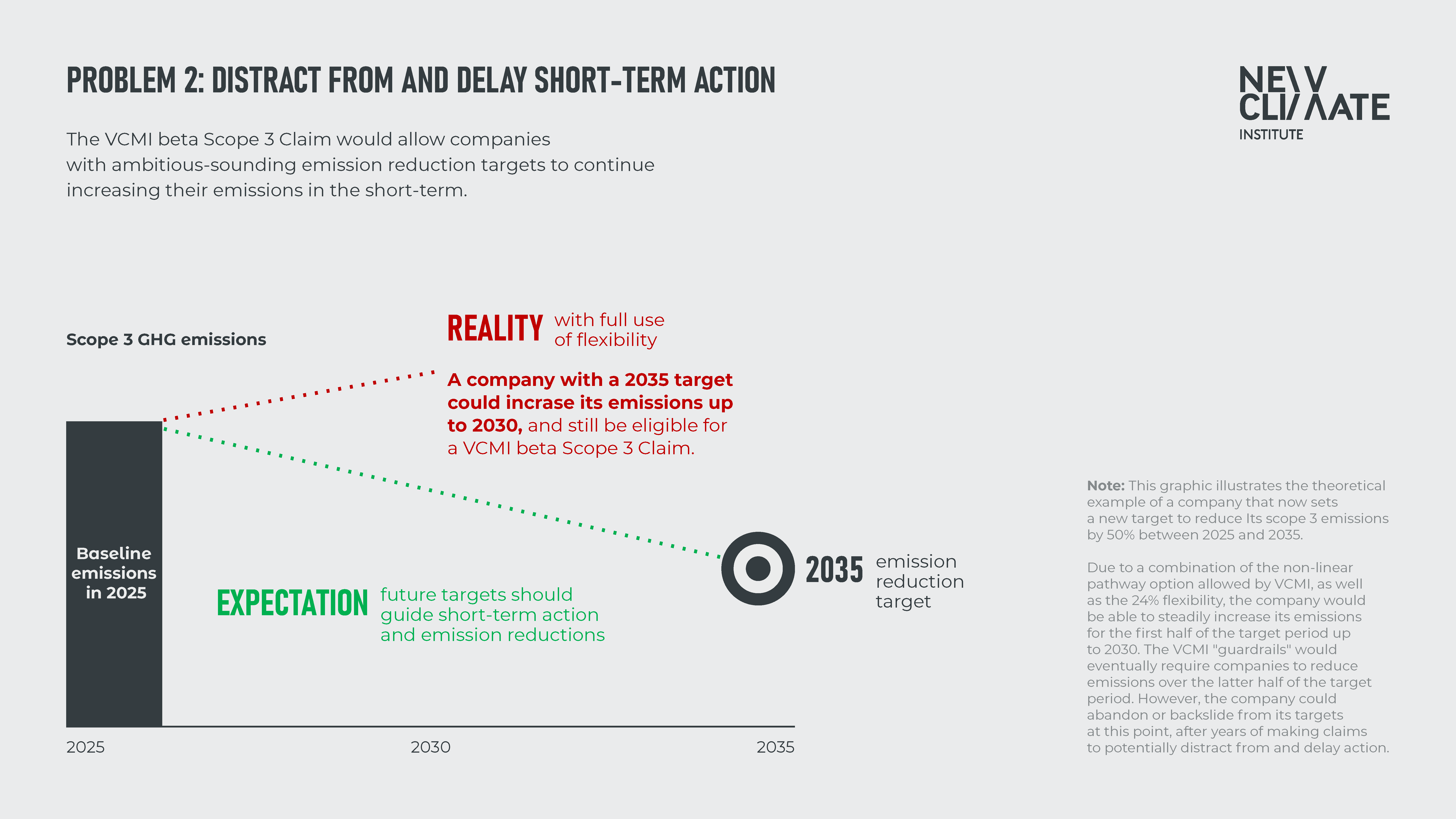

Problem 2: Distract from and delay short-term action

The VCMI proposal would allow companies with ambitious-sounding emission reduction targets to continue increasing their emissions in the short-term.

The implications of the Scope 3 Claim are even more severe for companies that may now set new targets for the future. Figure 2 illustrates an example of a company with a target to reduce its scope 3 emissions by 50% between 2025 and 2035. Due to the 24% flexibility allowance in addition to VCMI’s provision for companies to chart a non-linear pathway towards their targets, this company would be able to steadily increase its emissions for the first half of the target period up to 2030 while still qualifying for the VCMI Scope 3 Claim.

The VCMI’s so-called "guardrails" would eventually require companies to reduce emissions over the latter half of the target period. However, the company could simply abandon or backslide on its targets at this point, after benefitting from the flexibility for years. This could potentially allow the company to use the Scope 3 Claim to distract from and delay meaningful climate action.

Note: This graphic illustrates the theoretical example of company that now sets a new target to reduce its scope 3 emissions by 50% between 2025 and 2035. Due to a combination of the non-linear pathway option allowed by VCMI, as well as the 24% flexibility, the company would be able to steadily increase its emissions for the first half of the target period up to 2030. The VCMI "guardrails" would eventually require companies to reduce emissions over the latter half of the target period. However, the company could abandon or backslide from its targets at this point, after years of making claims to potentially distract from and delay action.

Problem 3: Undermining efforts of front-runners

The VCMI proposal could disadvantage ambitious companies with genuine climate strategies by allowing laggard competitors to exaggerate their own efforts.

The VCMI’s Scope 3 Claim creates a disincentive for companies to become first movers in implementing ambitious climate action that requires substantial financial and operational resources for its implementation, undermining efforts by leading companies to reduce emissions in the short-term such as Volvo Group, Mars or Iberdrola, among others. According to our analysis, these companies already implement ambitious climate actions along their value chains. For example, Volvo Group is currently implementing comprehensive measures to support the phase-in of electric vehicles by 2030 and taking credible steps to address upstream emissions by entering specific supply agreements for low-carbon steel (see Chapter 5.7 of 2024 Corporate Climate Responsibility Monitor for full analysis). Such measures require substantial investments for their short-term implementation, and first movers also face risks when implementing novel climate actions.

The VCMI’s Scope 3 Claim, however, enables laggard companies that have not undertaken similar efforts to misleadingly appear to be making similar progress towards ambitious-sounding targets. This may create a direct disincentive for companies to become first movers and put significant resources into tackling the considerable challenges of sectoral transitions. Moreover, it could penalise companies that have already committed to forward-looking investments and innovation under the assumption that offsetting would not be allowed. In this context, a growing number of companies are vocally opposing the use of carbon credits toward target fulfilment. [1]

VCMI’s Scope 3 Claim does not appear to align with the direction of the SBTi’s Corporate Net Zero Standard revision, which promises more transparent and constructive solutions.

Instead of succumbing to pressure to introduce unnuanced flexibility to its standards through carbon credits, the SBTi’s Scope 3 discussion paper – published in July 2024 – explores more direct and constructive solutions to address issues with corporate target setting.

The SBTi’s discussion paper sets out potential frameworks to encourage and enable companies to focus on critical emission sources through transition-specific alignment targets, rather than relying only on aggregated GHG metrics that are vulnerable to manipulation and creative accounting. For example, vehicle manufacturers may need to set near-term targets related to the annual sales share of zero-emission vehicles and the share of near-zero emission steel procured. In contrast to the controversial statement from the SBTi’s Board of Trustees in April 2024, the discussion paper reiterates SBTi’s position that carbon credits from activities outside the value chain should not count towards emission targets. This position is further supported by the SBTi’s Synthesis Report on carbon credits, which clearly points to the ineffectiveness of carbon credits to meet corporate climate targets.

VCMI’s Scope 3 Claim proposal overlooks these developments and contradicts the more innovative and nuanced direction of the SBTi’s revised Corporate Net Zero Standard. The International Standards Organisation (ISO) is also working on developing an international standard for corporate net zero targets.

Given these developments, we urge VCMI to abandon the proposed flexibility mechanisms that could undermine the progress of corporate net zero standards. Offsetting is an outdated approach: carbon credits should not be used as a flexibility mechanism to suggest that companies are on track to meet their targets or as sufficient compensation for failing to achieve them.

Short-term flexibility for corporations would delay necessary transitions and distract from their lack of progress—a fundamentally wrong approach to addressing the climate crisis. Companies must take immediate action to drastically reduce emissions within their value chains while developing long-term strategies for transitioning to net zero. We cannot afford any periods of inaction if we are to meet the goals of the Paris Agreement.

[1] See for example statements from H&M Group, Telstra, Decathlon, Michelin and other companies.