Although timely action on HFCs is likely to bring multiple benefits for end-users of cooling technologies, only few non-state actor driven initiatives exist yet that specifically target the refrigeration and air-conditioning (RAC) sector. It is important to address the barriers to non-state action in the RAC sector, while recognising that non-state action always needs to be accompanied by effective government policy and regulation to successfully address the climate challenge.

Abstract:

This paper seeks to inform policy makers and other stakeholders in partner countries of the Cool Contributions fighting Climate Change (C4) project and beyond about the potentials offered through both top-down and bottom-up approaches to promote effective mitigation action in the RAC sector. It looks at certain end-users of cooling technologies as important potential non-state actors whose technology choices can have significant impact on current and future RAC sector emissions. A focus is placed on three relevant end-users of RAC equipment: supermarkets, cold stores and hotels. Through in-depth sector studies, the paper provides a better understanding of the mitigation potential, ownership structures, technology options and decision-making processes prevalent in these industries. The analysis also looks at enhanced mobilisation and coordination of RAC sector related non-state action in C4 partner countries (Costa Rica, Grenada, Iran, Philippines, Vietnam). Key results of the study include the recognition that to date, only few non-state actor driven initiatives exist that specifically target the RAC sector. Yet, timely action on HFCs is likely to bring multiple benefits for end-users of cooling technologies. It is thus important to address the barriers that non-state actors face when engaging in mitigation action in the RAC sector, for example through the formation and support of alliances. At the same time, it must be kept in mind that non-state action is not a “silver-bullet” to the climate challenge, but needs to be accompanied by effective, mandatory regulation from the government.

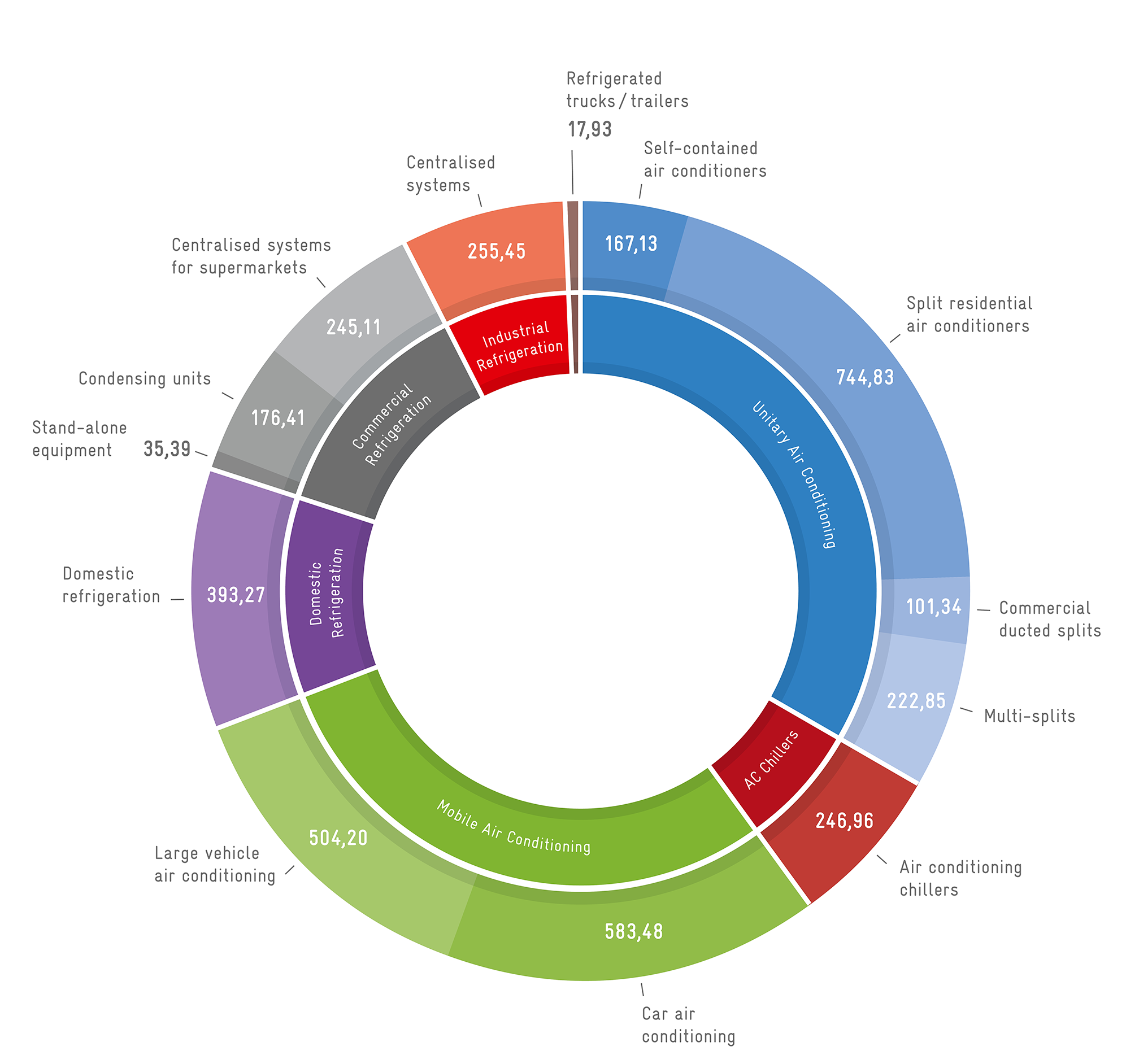

Estimated total emissions by system in 2015 in Mt CO2eq (Data: Green Cooling Initiative)

Conclusions:

- The Kigali Amendment and the Paris Agreement are different treaty regimes that offer potential or synergies in an effort to close the global emissions gap. Even though the exact impact of the Kigali Amendment in terms of emission reductions is still unclear, it can work alongside the Paris Agreement and provide an additional framework for mitigation by locking-in effective action on HFCs and energy efficiency, leading the way to the global 2°C goal.

- To date, top-down measures neither under the ozone nor under the climate regime have yielded the required results in terms of limiting global warming to 2°C. There is a need for enhanced bottom-up activity to fill the current emissions gap. Non-state action that goes beyond current regulatory and policy requirements set by national governments can play an important role in tapping the additional mitigation potential in the RAC sector.

- Important non-state actors in the RAC sector are end-users of cooling technologies. Through technology choices that take the use of natural refrigerants in refrigeration and air conditioning as well as energy efficiency into account, end-user industries can have a substantial impact on national GHG emissions and emission reductions in the RAC sector. In supermarkets, cold stores and hotels, RAC equipment is an important energy consumer that can be responsible for more than half of the overall energy consumption of a company. Apart from energy-related emissions, the leakage of high-GWP refrigerants causes additional emissions. Thus, the use of energy-efficient equipment with low-GWP refrigerants can substantially lower the carbon footprint of supermarkets, cold stores and hotels.

- So far, only a few bottom-up non-state actors or initiatives specifically target the RAC sector by defining explicit targets for HFCs or energy efficiency. Most information on bottom-up non-state actor activities is specific to certain sectors, such as supermarkets and food processing or beverage companies. For other RAC subsectors such as cold stores and hotels, only a few non-state actor initiatives target the RAC sector so far.

- Taking timely action on HFCs beyond what is mandated by national policies can bring multiple benefits for end-users of cooling technologies. Non-state action can help secure competitive advantages of being an ‘early mover’, mitigate profit risks caused by delayed action, derive economic savings from improved energy efficiency and increase reputational benefits which in turn can increase profits.

- Non-state actors still face many barriers and challenges when engaging in mitigation action in the RAC sector. These barriers can exist in the regulatory field, e.g. due to an unclear or restrictive policy environment; in the market and technology field, e.g. due to limited availability of alternative technologies or high upfront costs; or in the field of information and awareness, where a lack of knowledge on technology alternatives and their benefits may inhibit mitigation action. Governments have several options to address these barriers and actively increase participation from end-user industries in the RAC sector.

- Alliances can be powerful in supporting non-state action to leverage the full mitigation potential in the RAC sector. Networks of non-state actors can help monitor and analyse market trends, trade practices or legislative progress in a specific industry sector and encourage additional efforts for the introduction of alternative refrigerants and energyefficient technology in that sector.

- Policy makers, academia, and industry organisations can actively encourage greater participation of end-user industries in new or existing alliances. They can provide platforms, develop ideas and share knowledge and experiences, for example on the business case of refrigerant replacement and the adoption of energy-efficient cooling technologies. While supermarket and hotel operators often value reputational benefits, cold store operators are likely to be more susceptible to economic advantages since they are part of a complex supply chain and do not directly communicate a ‘green’ image to their customers.

- Non-state action has its limits! Voluntary non-state action is not per se more effective than mandatory regulation, and on its own it is rarely sufficient. Governments should seize the opportunity of non-state action in a specific industry sector to establish more ambitious policies that secure the progress made by non-state actors over the long-term.