Ambition to Action Phase II publication series

The three-part report series identifies transition risks faced by Argentina’s export-oriented agriculture industry (WP1), evaluates feasible emissions reduction options in the country’s livestock and cropping systems (WP2), and explores the potential economic opportunities associated with the global protein transition for the country and economy (WP3).

English:

Español:

Main findings:

The Argentinian agricultural sector plays a critical role for the country’s economy and its development trajectory. Argentina is one of the most important producers and exporters of agricultural commodities globally, specifically supplying soybeans and its derivatives, bovine meat, cereals, as well as dairy products to the world market. Agriculture, forestry, and other land use (AFOLU) sectors, including livestock farming and cropping systems, however, are not only of economic relevance for the country, but also contribute 37% of Argentina’s total greenhouse gas (GHG) emissions. Argentina’s agri-export model is the country’s economic backbone, but the sector’s growth targets are difficult to reconcile with the country’s stated climate ambition. Argentina has reiterated in its second Nationally Determined Contribution (NDC) the ambition to achieve climate neutrality by 2050. A credible pathway to climate neutrality requires all sectors of Argentina’s economy to start decarbonising today.

WP1: Transition risks for Argentina’s agriculture sector

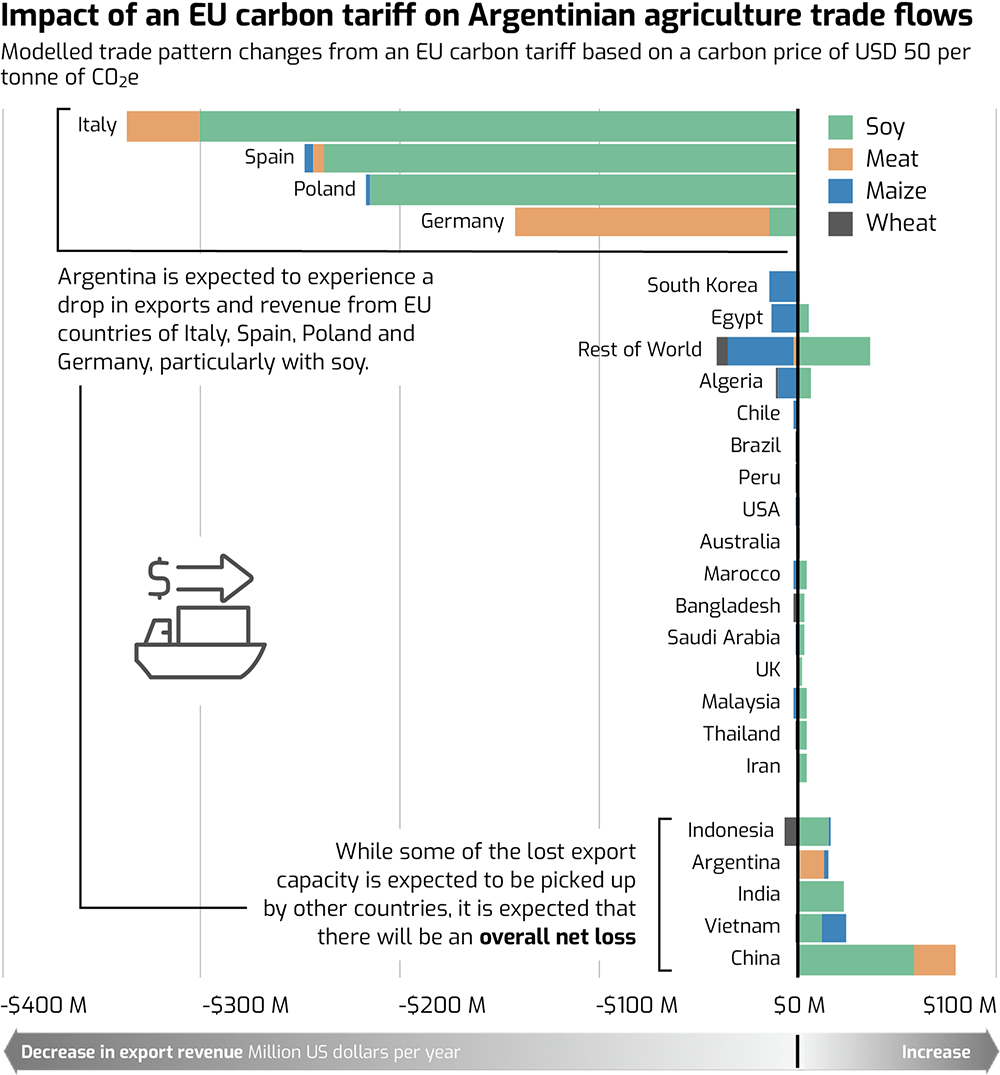

Given its GHG intensity and that of key commodities, the sector may face significant transition risks. More stringent environmental policy as well as changes in consumer preferences, domestically and in key export markets, are likely to affect Argentina’s agri-export model. The National Institute of Agricultural Technology (INTA) has conducted an industry survey to evaluate risk and impact perception of representative stakeholders vis-à-vis these transition risks. Survey results indicate that stakeholders generally do not expect more stringent climate commitments in domestic markets, but they acknowledge transition risks associated with more ambitious climate action and consumer preference change in third countries, especially in the EU. We attempt to monetize the risks of more stringent climate action in the EU by modelling the hypothetical introduction of an EU carbon tariff with full coverage of agriculture commodity imports. Results suggests that Argentina would incur significant economic losses in terms of forgone revenue already at moderate carbon tariff levels and that growth in Asian export markets is unlikely to compensate for lower EU demand.

Figure 1: Impact of an EU carbon tariff on Argentinian agriculture trade flows.

The necessary decarbonisation of global trade flows may represent an underestimated transition risk to Argentina’ economy. Taking early steps to reduce the GHG intensity of agricultural production systems, in turn, could represent a decisive source of competitive advantage for Argentina.

Download report / Descargar el informe

WP2: Climate change mitigation options for Argentina’s agriculture sector

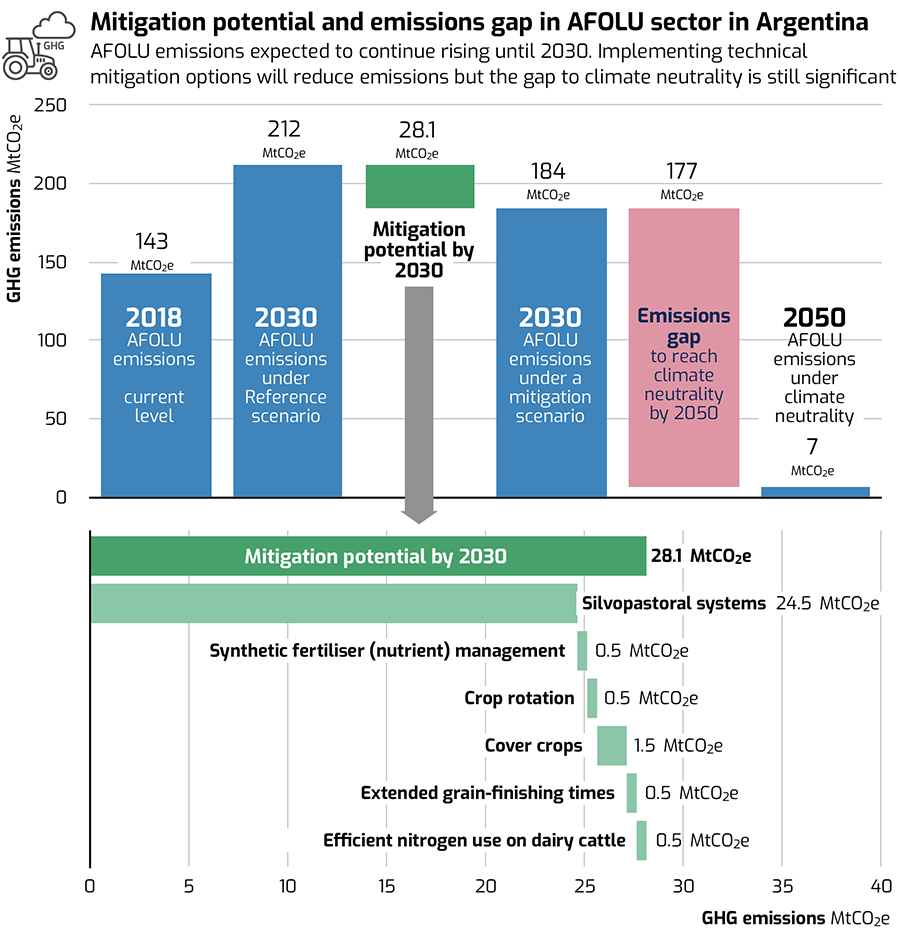

We evaluate a range of potential climate change mitigation measures in the agriculture sector in Argentina in close consultation with experts from INTA, based on available literature to support calculations, perception of feasibility of implementation, relevance in the national context and potential additional benefits. According to our findings, the implementation of key mitigation measures could reduce emissions by up to 14% in 2030 (~30 MtCO2e) compared to a reference scenario. Over 80% of the potential emissions reduction directly relate to halting deforestation for pastureland expansion. Even with a successful implementation of the measures evaluated in this report, the sector’s emissions pathway under a modelled mitigation scenario is misaligned with where it should be in 2030 to reach climate neutrality by 2050.

Figure 2: Mitigation potential and emissions gap in AFOLU sector.

By considering further mitigation measures that explore more fundamental transformations in the sector, Argentina could strengthen its position to reach its international climate commitments. Mitigation measures such as shifting to more sustainable diets (i.e. lower meat consumption) and reducing food waste reportedly have a high mitigation potential and are likely to provide significant co-benefits at relatively lower costs.

Download report / Descargar el informe

WP3: The global protein transition: An opportunity for Argentina

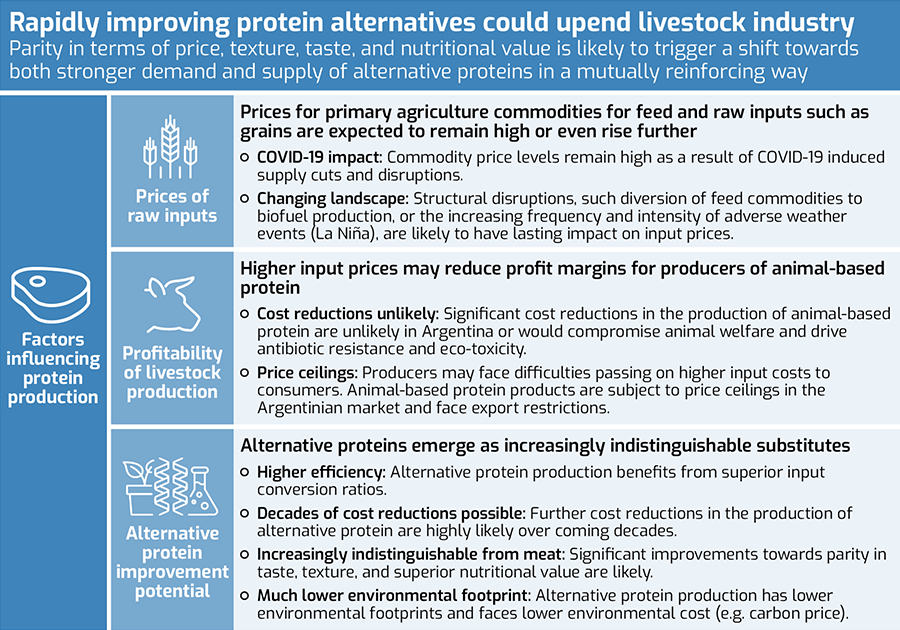

Argentina’s agriculture sector may need to undergo a deeper transformation. Globally, food systems are expected to increasingly shift away from a predominant reliance on animal-based protein towards more healthy and sustainable alternatives. Countries, and especially those with sizable livestock production sectors such as Argentina, will inevitably need to adapt to this global protein transition. Globally, per capita consumption of key meat commodities is projected to decline until 2030. This trend is expected to become more pronounced over time as motivational barriers fall. While the dynamics of changing consumer preferences may not pose a direct threat to producers and exporters of animal-based protein in the short-term, the emergence of near indistinguishable alternatives with clear advantages in terms of costs, health effects, and environmental footprints will inevitably cannibalize demand for animal-based protein.

Figure 3: Factors influencing protein production.

The protein transition also presents significant investment opportunities for Argentina. Plant-based products and lab-grown proteins are gaining traction and may make up between 11% and 22% of global protein consumption in 2035. Argentinian producers could put themselves at the forefront of the protein transition, by targeting technological challenges along the plant-based and cultivated protein value chains, as well as by utilizing existing industrial capacity and capital to reach scale in commercial production. By promoting the development of a strong domestic alternative protein industry and a shift away from animal-based protein production, the public sector can promote export diversification and reduce transition risks, reduce negative externalities of conventional protein production systems, drive domestic value creation and employment, and unlock social welfare gains.